By WRAL TechWire | March 13, 2018

DURHAM – A new study from the Iqvia Institute for Human Data Science forecasts that technology, such as mobile apps, telehealth and biotherapeutics, will continue to have a huge impact on solving what it calls “the problems of human health.”

Iqvia, the global life science services firm that operates twin headquarters in Durham and Connecticut, makes 10 predictions that researchers say “promise to transform healthcare cost and spending, drug development and delivery, and approaches to determine the societal value of medicines.”

Some of the predictions “will begin to come to pass later this year,” says Murray Aitken, executive director of the IQVIA Institute for Human Data Science, in the study, which is being released Tuesday.

“HARBINGERS OF HEALTHCARE TRANSFORMATION”

The 10 “harbingers of healthcare transformation” follow:

- FDA to guide the use of Real-World Evidence (RWE) to support regulation of medicines:

In 2018, FDA will issue its first framework addressing the potential for RWE to support regulatory submissions and drug safety monitoring. As big data gathered in real-world healthcare settings becomes more prevalent and robust, it is increasingly being used across the entire healthcare system for evidentiary purposes. With this shift, regulators will be both enabled and challenged to accelerate the pace of their review through new data-derived protocols, insights and approaches. It’s expected that this evidence, paired with existing clinical trial data, will foster more collaborative approaches between life sciences companies and the FDA around areas such as trial design and post-market surveillance.

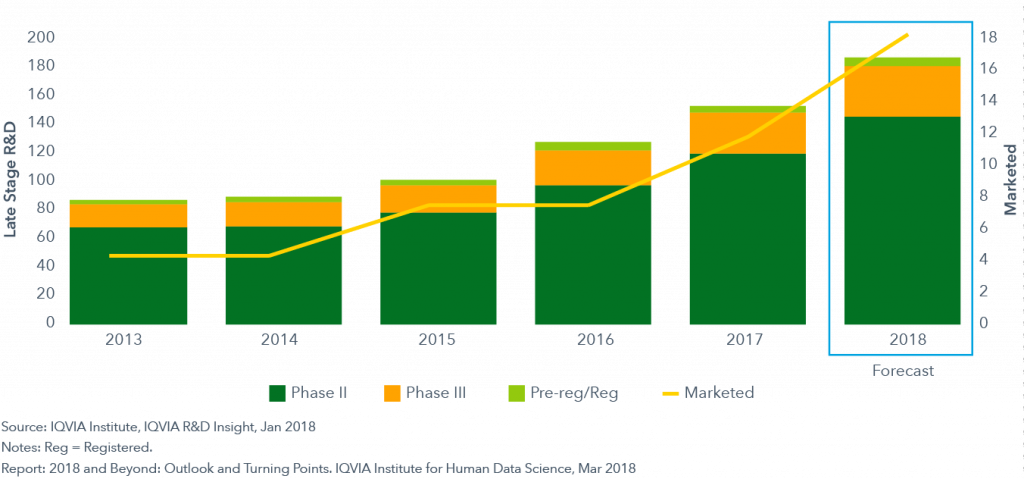

- Niche biotherapeutics move toward mainstream:

Forecast growth of biotherapeutics

From 2018 through 2022, between five to eight new therapies will launch each year within a new generation of cell-based therapies, gene therapies and regenerative medicines. This wave of Next Generation Biotherapeutics will stretch the definition of a “drug” as we know it. Some are engineered for individual patients, while others transform previously untreatable or chronic diseases with curative results in a single dose. Others upend spending paradigms because they carry an extremely high cost per patient relative to traditional therapies. Providing access to these clinical advances will be a challenge for governments and insurers without methods to determine which patients are eligible for treatments, negotiated payments based on outcomes, or ability to spread costs over time.

- Mobile health apps will be added to treatment guidelines:

Treatment guidelines from major clinical organizations will adopt and recommend the use of mobile health apps this year – some already have done so. The trend toward developing and publishing hard evidence of the value of digital tools and interventions will continue with more than 3,500 studies expected through 2022. The emergence of well-designed apps and mobile devices has paralleled the development of rigorous clinical trial evidence supporting their value. As mobile apps are better integrated into provider workflows and supported by payer reimbursement, adoption will expand further. These advances offer the potential to improve outcomes for patients sometimes at near-zero incremental costs. While alignment on the appropriate sets of features and safeguards has taken time to develop, there is growing consensus and technology innovators are advancing into the field in significant numbers.

- Use of telehealth will expand:

Nearly every privately insured patient in the U.S. will have some form of access to telehealth this year, though few will use it. In 2018, telehealth visits will account for 3-3.5 percent of visits, up from 2.6 percent in 2017. Over the next five years telehealth will grow between 4 and 7.5 percent of visits as patient concerns about being treated by a random doctor are outweighed by the dramatically lower copayments offered by their insurers. Advocates of telehealth argue that most of the reasons to see a provider in person can be supported remotely. For payers, concerns about measurable benefits and/or potential fraud are being addressed by technology and are outweighed by cost savings relative to inappropriate use of emergency or urgent care.

- Spending on branded medicines will dip:

In 2018, net brand spending will decline in developed markets by 1-3 percent. This has the effect of reducing net spending overall on brands in developed markets by approximately $5 billion, to a total of $391 billion for this year. Net brand spending will remain flat in the next five years, despite the expected entry of new branded medicines. The overall impact on payers, however, should be the same in 2022 for brands as it was in 2017. Manufacturers will continue to develop and launch drugs, but the inherent unpredictability of medicines spending will drive continued caution among payers regarding reimbursement and access.

- Specialty brands will drive growth in developed markets:

In 2018, the $318 billion specialty medicines market will represent 41 percent of developed market spending, up from $172 billion in 2013. In fact, specialty drugs will contribute all of the growth in medicine spending in 2018, however, those increases will be offset by spending declines in traditional therapies. The growth of spending on specialty medicines will be constrained by cost and access controls and a greater focus on assessments of value. Despite these trends, specialty brands are expected to reach 48 percent of total spending in developed markets by 2022.

- Slower growth across pharmerging markets:

Growth in pharmerging markets will slow to 7-8 percent in 2018, down from the 9.7 percent compound annual growth rate over the prior five years. This will mark the third year that growth will be less than 10 percent. The IQVIA Institute for Human Data Science defines pharmerging countries as those with per capita income below $30,000 and a five-year aggregate pharmaceutical growth of more than $1 billion. The share of global medicine spending from pharmerging markets rose from 13 percent in 2007 to 24 percent in 2017. The markets within these pharmerging countries are projected to grow by 6-9 percent to $345-375 billion by 2022, driven by volume changes and the use of generics. Overall, the progress of advancing global health will continue, but the gains in access to medicine over the past decade will not continue at the same pace due to slowing economic growth within this key group of countries.

- U.S. net per capita spending will stabilize:

Real net per capita spending on medicines in the U.S. will decline in 2018 and continue almost unchanged at roughly $800 per person through 2022. Spending will remain flat after factoring in the robust pipeline of new drugs, moderating brand price increases of 2-5 percent on a net basis (7-10 percent on a list price basis) and the impact of brand losses of exclusivity, which will be greater in the next five years than the last five. While setting prices freely has been a unique feature of the U.S. market compared to other countries, the leverage payers have to negotiate net price discounts is effectively offsetting price increases.

- Outcomes-based contracts will play limited role:

The basic framework for an outcomes-based contract contains a payment schedule based on how well a drug does or doesn’t deliver results. The most common approach is for insurers to pay less for a drug if it performs worse than the reported results from its clinical trial for FDA approval and pay more for better results. Under these contracts, successful medicines get covered at full price or for proportionately less based on unsuccessful patient results. These contracts can drive real savings for payers or providers, as well as more predictability for overall costs. As the health system gains a greater comfort with electronic medical records, as well as wider use of RWE, collecting data for these outcome requirements will become easier. However, the administrative burden on all parties will escalate and become prohibitive unless the outcomes are designed to be measurable.

- New wave of biosimilar competition and opportunity emerges:

In 2018, $19 billion of current biotech spending in developed markets will have competition from biosimilars for the first time. That amount is significantly greater than the $3 billion in biosimilar revenue that became exposed in 2017, and it adds to the $26 billion already facing competition. The new exposure to competition in 2018 is the largest single-year change to date and signals the start of the next large wave of biosimilars. The benefits of a functioning biosimilar market include expanding access and cost savings across public and private healthcare systems. While overall it appears that the next decade will provide sufficient incentives to encourage biosimilar challengers, the greatest uncertainty around biosimilars is whether all medicines that can be challenged in the next decade will indeed face competition and from how many companies.

The full report can be read online.

According to the institute, the study was “produced independently as a public service, without industry or government funding.”